BSA & AML Risk Assessment

A BSA/AML Risk Assessment is a regulatory-required evaluation identifying your business’s exposure to money laundering, terrorist financing, and financial crime risks.

If you operate as: An MSB, FinTech, crypto exchange, payment processor, money transmitter, or any financial service provider

What Is a BSA/AML Risk Assessment?

A BSA/AML Risk Assessment is a comprehensive analysis that:

- Identifies inherent money laundering and terrorist financing risks

- Evaluates control effectiveness

- Determines residual risk exposure

- Documents risk mitigation strategies

- Provides regulator-ready documentation

Required under:

- Bank Secrecy Act (BSA)

- FinCEN AML Program Rule

- State money transmitter regulations

- Banking partner requirements

- FFIEC BSA/AML standards

Who Needs a BSA/AML Risk Assessment?

Money Service Businesses (MSBs)

FinCEN requirement:

- All registered MSBs must conduct enterprise-wide risk assessments

- Core component of effective AML program

- Updated periodically based on business changes

Money Transmitter License Applicants

State regulator requirement:

- Comprehensive risk assessment in license applications

- Demonstrates understanding of ML/TF exposure

- Required for license approval

FinTech & Payment Companies

Banking partner requirement:

- Sponsor banks demand current risk assessments

- BaaS providers require annual updates

- Payment processors verify risk management

Companies Facing Regulatory Examinations

FinCEN & state examiner focus:

- Risk assessment quality reviewed during examinations

- Deficient assessments trigger enforcement

- Must align with business model and operations

![Who needs risk assessment]

What We Assess: Five Core Risk Categories

1. Products & Services Risk

We analyze:

- Payment types (ACH, wire, P2P, crypto)

- Transaction speed and anonymity

- Cross-border capabilities

- Product complexity

Higher-risk products:

- International wire transfers

- Cryptocurrency exchanges

- Prepaid cards with cash reload

- Anonymous payment methods

2. Customer Risk

We evaluate:

- Customer types (individual, business, institutional)

- Occupation and industry sectors

- Expected transaction patterns

- Source of funds

Higher-risk customers:

- Politically Exposed Persons (PEPs)

- Cash-intensive businesses

- MSBs and money transmitters

- Cryptocurrency businesses

3. Geographic Risk

We examine:

- Customer locations

- Transaction destinations

- High-risk jurisdictions (FATF, FinCEN)

- Sanctions countries

Higher-risk geographies:

- FATF high-risk jurisdictions

- OFAC sanctioned countries

- Known drug trafficking regions

Terrorist financing locations

4. Transaction Channels

We review:

- Online/mobile platforms

- In-person locations

- Agent networks

- API integrations

Higher-risk channels:

- Non-face-to-face onboarding

- Agent networks with limited oversight

- Third-party processors

5. Transaction Volume & Velocity

We analyze:

- Dollar volume by product

- Transaction frequency

- Velocity thresholds

- Unusual patterns

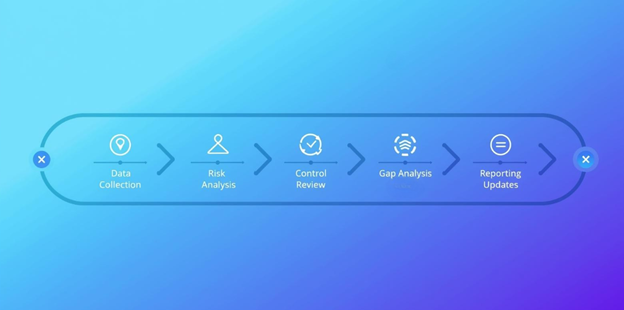

Our BSA/AML Risk Assessment Process

Step 1: Data Collection

- Business model documentation

- Customer demographics

- Transaction data and patterns

- Geographic footprint

- Current policies and procedures

Step 2: Inherent Risk Analysis

- Identify ML/TF risks by product

- Customer segment risk profiles

- Geographic exposure

- Channel vulnerability

Step 3: Control Effectiveness Review

- Customer due diligence procedures

- Transaction monitoring systems

- Sanctions screening

- Suspicious activity detection

- Training effectiveness

Step 4: Residual Risk Determination

- Calculate residual risk after controls

- Gap analysis

- Control enhancement priorities

- Resource allocation recommendations

Step 5: Documentation & Reporting

- Comprehensive written risk assessment

- Executive summary for board

- Risk matrices and heat maps

- Remediation recommendations

Step 6: Ongoing Updates

- Annual reassessment (minimum)

- Updates for business changes

New product risk evaluations

Why BSA/AML Risk Assessment Matters

Regulatory Compliance

- Federal and state law requirement

- Foundation of risk-based AML program

- Demonstrates compliance commitment

Examination Preparedness

- Shows regulators you understand your risks

- Documents control rationale

- Reduces examination findings

Banking Relationships

- Banks require current assessments

- Prevents account closure

- Demonstrates risk management maturity

Strategic Decisions

- Informs product launch risk

- Guides geographic expansion

- Supports customer segmentation

Regulatory Standards We Meet

FinCEN Requirements

- Risk-based compliance approach

- Assessment of ML/TF risks

- Documentation of methodology

- Board and management awareness

FFIEC BSA/AML Standards

- Comprehensive risk assessment

- Appropriate methodology

- Board involvement

- Control alignment with risks

State Money Transmitter Regulations

- Risk assessment in applications

- Annual updates

- Board-approved documentation

Banking Partner Expectations

- Current assessments (within 12 months)

- Evidence of board approval

- Control alignment documentation

- Annual certification